When you boil it down, ‘compounding’ refers to growth on top of growth, or to put it another way, exponential growth... It doesn’t sound too confusing, does it? I expect you’re shrugging and saying “so what? Any idiot can understand that concept”, and you’d be half right. You see, the human brain is a very weird squishy machine and while we can grasp concepts at a high level, we often fail to understand what it actually means in reality, and compounding is definitely one of those ideas.

Allow me to illustrate this phenomenon by borrowing my favourite example from economic researcher Chris Martinson…

Suppose I had a magic eye dropper and I placed a single drop of water in the middle of your left hand. The magic part is that this drop of water is going to double in size every minute.

At first nothing seems to be happening, but by the end of a minute, that tiny drop is now the size of two tiny drops.

After another minute, you now have a little pool of water that is slightly smaller in diameter than a dime sitting in your hand.

After six minutes, you have a blob of water that would fill a thimble.

Now suppose we take our magic eye dropper to Fenway Park, and, right at 12:00 p.m. in the afternoon, we place a magic drop way down there on the pitcher’s mound.

To make this really interesting, suppose that the park is watertight and that you are handcuffed to one of the very highest bleacher seats…

My question to you is, “How long do you have to escape from the handcuffs?” When would it be completely filled? In days? Weeks? Months? Years? How long would that take?

I’ll give you a few seconds to think about it.

The answer is, you have until 12:49 on that same day to figure out how you are going to get out of those handcuffs. In less than 50 minutes, our modest little drop of water has managed to completely fill Fenway Park.

Now let me ask you this – at what time of the day would Fenway Park still be 93% empty space, and how many of you would realize the severity of your predicament?

Any guesses? The answer is 12:45. If you were squirming in your bleacher seat waiting for help to arrive, by the time the field is covered with less than 5 feet of water, you would now have less than 4 minutes left to get free.

And that, right there, illustrates one of the key features of compound growth…the one thing I want you take away from all this. With exponential functions, the action really only heats up in the last few moments.

We sat in our seats for 45 minutes and nothing much seemed to be happening, and then in four minutes – bang! – the whole place was full.

With this example now fresh in our mind, we can see how this concept can apply to all kinds of scenarios. For example, the Covid pandemic is a perfect recent example of exponential growth where the problem got radically worse the further we moved along the right-hand side of the graph. Take a look at the UK covid case-count up until the peak in December 2020…

It’s clear to see that towards the right of the graph the situation became drastically more dire and very rapidly got away from the UK government’s control. This is because Boris Johnson and his team underestimated the effect of compounding. I absolutely blame him, but it is also true that it is human nature to underestimate this phenomenon (as you yourself learned with the baseball stadium example above).

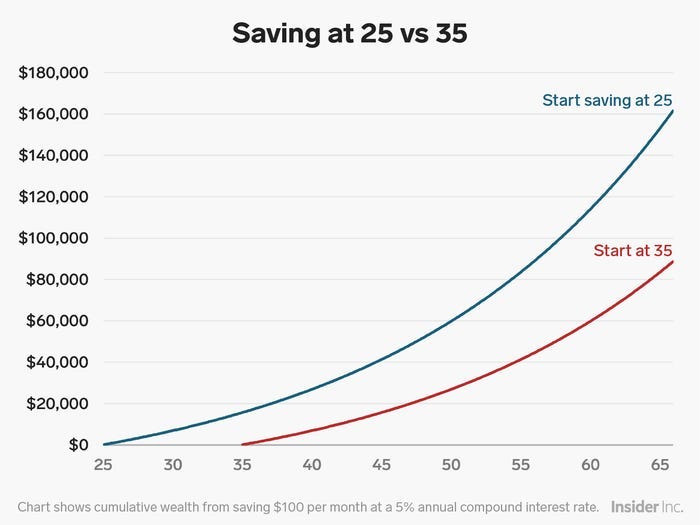

Our job as investors is to comprehend compounding. Arm yourself with the knowledge that the longer you can leave something to compound the greater the exponential return. Put another way, the younger you are when you start investing the wealthier you will become. Think about what compounded returns will mean for you when you’re 65 or ready to retire Here’s a simple illustration from Business Insider showing what $100 a month put away with a 5% return looks like if you start at age 25 vs 35. As you can see the 25-year-old investor retires with $160,000 while the 35-year-old investor ends up retiring with just $85k. That is a massive delta caused by a mere ten-year headstart.

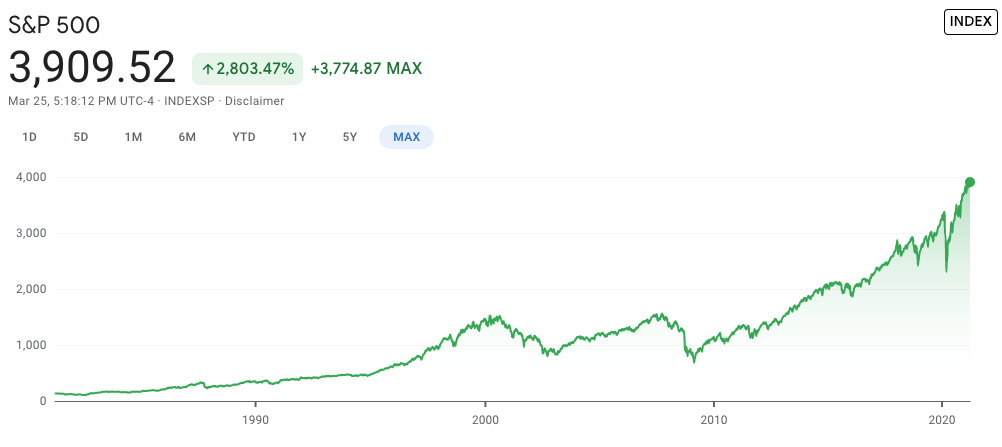

You’re probably thinking “Well damn… What do I do now?”. Well, you need to build a pot of cash that you can afford to stash away for decades and you need to find a source of growth or yield. Interest rates on saving accounts at the bank are essentially non-existent so your best bet is going to be something with some risk attached, like stocks. The S&P500 (an index that represents the 500 biggest US companies) has historically given an average annual return of around 10% since it was created in 1926…

As you can see there have been some brutal drawdowns (the 2000 dotcom bubble, the 2008 great financial crisis) but on a long time horizon you can clearly see that stocks move up and to the right. Therefore with decades on your side an S&P500 ETF would be a relatively safe place to park your savings, assuming you’re able to leave it untouched. This would certainly give you the desired compounding effect. This is just one example of how you may want to invest, you could also pick your own stocks or invest in any other number of equities and assets based on your risk tolerance (Bitcoin, property etc). What matters most is how much time you can leave it to compound. They weren’t lying, time really is money.

Like this post? Hit that subscribe button and get my posts directly in your inbox each week…

Not an investor yet but interested to try? I recommend using the FreeTrade app which is free (no commissions on buy or sell), lets you get started with just a couple of pounds and is perfect for newcomers with an easy to use interface. Use this Loot Box Investing referral link and we both get a free random stock when you sign up.