“Oh my God, Oh God no! Oh this can’t be happening!" - The UK's Inflation Problem

“Oh my God, Oh God no! Oh this can’t be happening!" - The UK's Inflation Problem

If you thought 5% interest rates on mortgages were painful you'd better brace yourself

There is a sensational scene in season 7 (1989!) of The Simpsons where, in an effort to help get Bart home Homer purposefully breaks a console at his workstation at the Nuclear Power Plant so that he can get a new one shipped to Springfield. He pours a can of cola across the console as the voice of the expert on the line starts to freak out…

“Oh my God, Oh God no! Oh this can’t be happening! You’re operating without a T-437 Springfield! Sweet mother of mercy! I mean… I mean my God!”

The gag is perfect and Hank Azaria’s delivery is pure genius. The reason I bring this scene up is because the UK’s core inflation data for May just came in and despite twelve successive interest rate hikes by the Bank of England, core CPI went up!

“Oh my God, Oh God no! Oh this can’t be happening!

This is a pretty terrifying set of data for the boffins because it confirms what I feared in September last year…

How the heck are our governments and central banks going to get inflation under control without bankrupting their own countries?…

So far as I can tell, the current plan is to try and maintain credibility by gradually hiking rates while hoping that global supply chains ease and the war in Ukraine ends such that inflation organically comes down by itself. I’m not sure I can put faith in a strategy that boils down to hoping things improve.

Hoping for circumstances to change hasn’t worked. Britain is still Brexited. Russia is still invading Ukraine and a decade+ of dreadful government policy is still compounding on itself. Inflation isn’t going anywhere.

With history as a guide, historically in the West the only way to bring this kind of sticky inflation down is by brute force, and by brute force, I mean taking interest rates up until they are higher than the inflation reading itself. So if your inflation sits at 8.7%? To brute force that down you need interest rates higher than 8.7%, so 9.5% sort of thing.

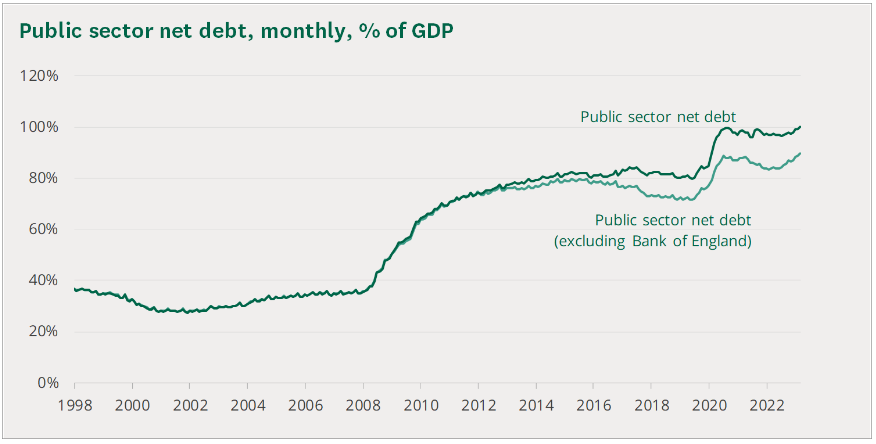

10% interest rates used to not break things back in the day because the level of debt was relatively manageable. The next chart is from the Government Commons Library and shows you public net debt as a percentage of GDP over time…

As you can see the UK’s debt is currently exceeding 100% of GDP (for the first time since the 1960s as CityAM helpfully points out). Paying 10% interest isn’t too bad when you’ve only borrowed £10. Most folks can find the extra quid. Paying 10% interest when you’re £2.5 trillion in the hole… Kinda different.

The housing market is the obvious pinch point. During the pandemic the government propped the property market up with a stamp duty holiday, the cut-off for which was 30th September 2021. That incentivised a lot of folks to buy property and take out a mortgage… many of those will have been two year fixed rate deals. Well, here we are a few months away from the two year anniversary of that scheme and those folks will all need to refinance. Estimates suggest around 800,000 fixed-rate deals are set to come to an end in the latter half of this year. Will home owners be able to shoulder interest rates two or three times higher than they expected when they first bought? We won’t have to wait too long to find out but odds are on for higher rates of repossessions and decreasing house prices.

Under any other circumstances this is when the government would swoop in with some kind of support scheme, however to do so in this situation would undermine the BoE’s attempts to fight inflation, so homeowners are probably going to be on their own.

So what do we have? We have an economy with record levels of debt. A population that has made their property the lion share of their net worth, inflation thats going nowhere but up and a central bank with almost no choice but to purposefully cause a recession.

“Oh my God, Oh God no! Oh this can’t be happening! You’re operating without central bank support, Britain! Sweet mother of mercy! I mean… I mean my God!”

Like this post? Hit the subscribe button and get my posts directly in your inbox.

Not an investor yet but interested to try investing in stocks? Check out my beginner’s guide. I recommend using the FreeTrade app which is free, lets you get started with just a couple of pounds and is perfect for newcomers with an easy to use interface. Use this Loot Box Investing referral link and we both get a free random stock when you sign up.

Agree or disagree with any of the above? Love or hate this? Let me know on Twitter - @LootBoxInvest.